To: The Voting Public

From: Prime Minister of Eurozone Periphery Country

My fellow citizens,

We have been telling you for the past six years that the reason you are out of work and that the next decade will be miserable is that states have spent too much. So now we all need to be austere and return to something called “sustainable public finances.” It is, however, time to tell the truth.

We have been telling you for the past six years that the reason you are out of work and that the next decade will be miserable is that states have spent too much. So now we all need to be austere and return to something called “sustainable public finances.” It is, however, time to tell the truth.

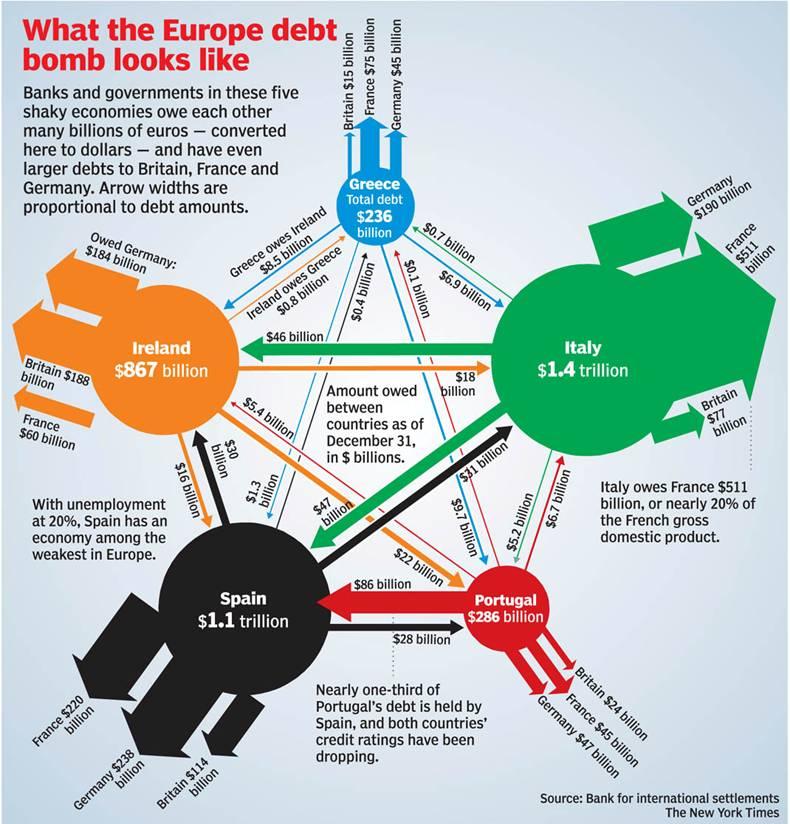

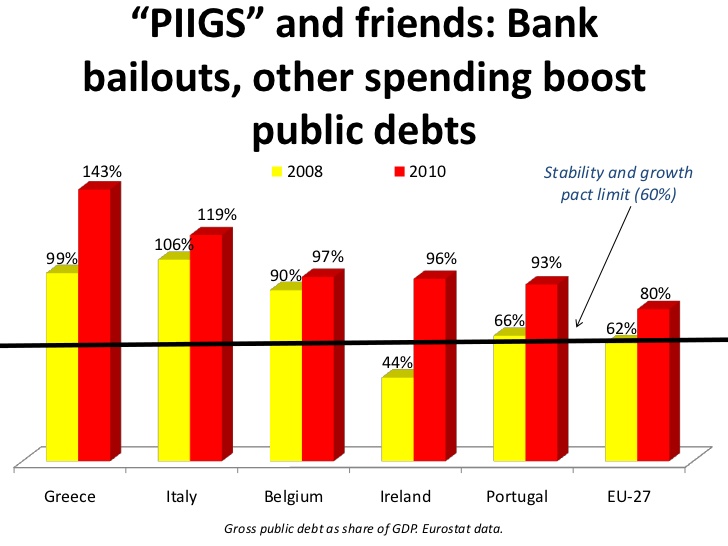

The explosion of sovereign debt is a symptom, not a cause, of the crisis we find ourselves in today. What actually happened was that the biggest banks in the core countries of Europe bought lots of sovereign debt from their periphery neighbors, the PIIGS (Portugal, Italy, Ireland, Greece and Spain). This flooded the PIIGS with cheap money to buy core country products, hence the current account imbalances in the Eurozone that we hear so much about and the consequent loss of competitiveness in these periphery economies. After all, why make a car to compete with BMW if the French will lend you the money to buy one?

This was all going well until the markets panicked over Greece and figured out via our “kick the can down the road” responses that the institutions we designed to run the EU couldn’t deal with any of this. The money greasing the wheels suddenly stopped, and our bond payments went through the roof. The problem was that we had given up our money presses and independent exchange rates— our economic shock absorbers—to adopt the euro.

Meanwhile, the European Central Bank, the institution that was supposed to stabilize the system, turned out to be a bit of fake central bank. It exercises no real lender-of-last-resort function. It exists to fight an inflation that died in 1923, regardless of actual economic conditions. Whereas the Fed and the Bank of England can accept whatever assets they want in exchange for however much cash they want to give out, the ECB is both constitutionally and intellectually limited in what it can accept. It cannot monetize or mutualize debt, it cannot bail out countries, it cannot lend directly to banks in sufficient quantity. It’s really good at fighting inflation, but when there is a banking crisis, it’s kind of useless. It’s been developing new powers bit-by-bit throughout the crisis to help us survive, but its capacities are still quite limited.

Now, add to this the fact that the European banking system as a whole is three times the size and nearly twice as levered up as the US banking system; accept that it is filled with crappy assets the ECB can’t take off its books, and you can see we have a problem. We have had over twenty summits and countless more meetings, promised each other fiscal treaties and bailout mechanisms, and even replaced a democratically elected government or two to solve this crisis, and yet have not managed to do so. It’s time to come clean about why we have not succeeded.

The short answer is we can’t fix it. All we can do is kick the can down the road, which takes the form of you suffering a lost decade of growth and employment. You see, the banks we bailed in 2008 caused us to take on a whole load of new sovereign debt to pay for their losses and ensure their solvency. But the banks never really recovered, and in 2010 and 2011 they began to run out of money. So the ECB had to act against its instincts and flood the banks with a billion euros of very cheap money, the LTROs (the long-term refinancing operations), when European banks were no longer able to borrow money in the United States. The money that the ECB gave the banks was used to buy some short-term government debt (to get our bond yields down a little), but most of it stayed at the ECB as catastrophe insurance rather than circulate into the real economy and help you get back to work. After all, we are in the middle of a recession that is being turbocharged by austerity policies. Who would borrow and invest in the midst of that mess?

The entire economy is in recession, people are paying back debts, and no one is borrowing. This causes prices to fall, thus making the banks ever more impaired and the economy ever more sclerotic. There is literally nothing we can do about this. We need to keep the banks solvent or they collapse, and they are so big and interconnected that even one of them going down could blow up the whole system. As awful as austerity is, it’s nothing compared to a general collapse of the financial system, really. So we can’t inflate and pass the cost on to savers, we can’t devalue and pass the cost on to foreigners, and we can’t default without killing ourselves, so we need to deflate, for as long as it takes to get the balance sheets of these banks into some kind of sustainable shape. This is why we can’t let anyone out of the euro. If the Greeks, for example, left the euro we might be able to weather it, since most banks have managed to sell on their Greek assets. But you can’t sell on Italy. There’s too much of it. The contagion risk would destroy everyone’s banks.

So the only policy tool we have to stabilize the system is for everyone to deflate against Germany, which is a really hard thing to do even in the best of times. It’s horrible, but there it is. Your unemployment will save the banks, and in the process save the sovereigns who cannot save the banks themselves, and thus save the euro. We, the political classes of Europe, would like to thank you for your sacrifice.

This is a speech that you will never hear because if it were given the politician making it would be putting a resume up on Monster.com ten minutes later. But it is the real reason we all need to be austere. When the banking system becomes too big to bail, the moral hazard trade that started it all becomes systemic “immoral hazard”—an extortion racket aided and abetted by the very politicians elected to serve our interests. When that trade takes place in a set of institutions that is incapable of resolving the crisis it faces, the result is permanent austerity.

This post is an extract from Blyth, Mark (2013-03-27). Austerity: The History of a Dangerous Idea (p. 88). Oxford University Press.

Pingback: Fim do Sistema Babilónico de Escravização pelo Dinheiro – Anatomia da Consciência