Part 1 by Ed Nolan (EconoMonitor)

The news that Switzerland will hold a referendum on a proposal to provide every citizen with an unconditional grant of 2,500 Swiss francs a month (about $2,800) has sparked renewed interest in the old idea of a universal basic income (UBI). Under such a program, the government would not just top up the incomes of the poor, but would give a subsistence-level grant to everyone, regardless of wealth, work status, or anything else. The appeal of a UBI seems to cut across the ideological spectrum. Progressives, libertarians, and conservatives have all supported one or another variant.

This post begins a series that will explore various aspects of a universal basic income, beginning with the simple economics of the UBI and contrasting it with other approaches to income support. Future posts will examine the fiscal cost of a UBI and some of the political and ideological issues it raises.

Criteria for evaluating income support systems

What makes an income support program good or bad? Although opinions differ, people who evaluate existing or proposed policies often appeal to these four criteria:

- A good income support program should be effective in leaving no one below an agreed poverty level.

- It should be targeted in the sense that it should provide support to those who need it rather than to those who already have adequate means.

- It would, as much is possible, leave work incentives intact.

- It would be administratively efficient, in the sense of holding down administrative costs per dollar of support that beneficiaries receive.

Unfortunately, no income-support mechanism can simultaneously meet all of these criteria in full. There are inherent trade-offs among them. Let’s take a look at the different ways that actual and proposed policies handle those trade-offs.

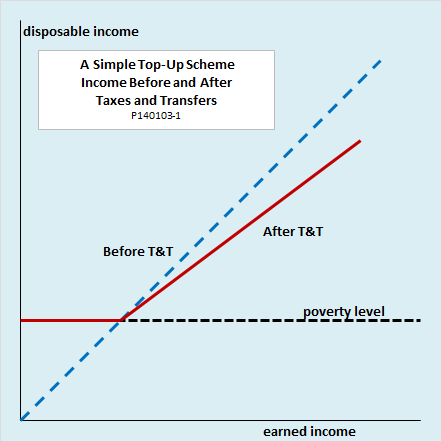

A simple top-up

The simplest income transfer system would be a commitment to top up the income of each household to, but not above, the poverty level. (See this earlier post for a review of some of the issues in defining and measuring poverty. Official U.S. poverty guidelines for 2013 are about $20,000 for a family of three, a figure I will use for the sake of illustration whenever a numerical example seems helpful.) The following diagram shows the effects of a simple means-tested top-up.

The horizontal axis shows the income that the household earns. The vertical axis shows its disposable income after payment of taxes and receipt of transfer payments. The dotted line labeled “Before T&T” shows that without any taxes or transfer payments, disposable income would equal earned income. The solid line “After T&T” shows the effects of taxes and transfer payments. The diagram assumes a 20 percent income tax on all earned income above the poverty level, so the “after” line lies below the “before” line for households who are subject to the tax. Households with lower earned incomes receive a cash transfer payment sufficient to bring their disposable income up to the poverty level.

The simple top-up approach scores well by the first two of our criteria. It is 100 percent effective, in that it leaves no one with a disposable income below the poverty line. Also, it is well targeted. No payments go to households whose earned incomes alone would lift them above the poverty line, and no transfer beneficiary receives more than is needed to reach the poverty level. However, the simple top-up scheme scores poorly in other respects.

In particular, it provides poor work incentives. Three terms are helpful in understanding how transfers affect work incentives:

- The benefit reduction rate for a program is the amount by which benefit payments fall for each add dollar of earned income.

- The marginal tax rate is the amount by which tax payments increase for each added dollar of earned income.

- The effective marginal tax rate is sum of the benefit reduction rate and the marginal tax rate. For example, if benefits are reduced by 25 cents for each dollar earned and if the marginal tax rate on earned income is 20 percent, then the effective marginal tax rate is 45 percent. In that case, disposable income after taxes and transfers would rise by just 55 cents for each add dollar of earned income.

As the diagram shows, the simple top-up scheme imposes a benefit reduction rate (and effective marginal tax rate) of 100 percent on poor households, leaving them little incentive to work at all. Work incentives are also weak for those just above the poverty line. True, at the margin, such households can keep 80 cents of each added dollar of income, but varying income by a dollar at a time is not always feasible. Instead, people will often face the choice between taking a job for a set number of hours per week, or remaining unemployed.

Suppose, for example, that the poverty line is $20,000 and one person in the household gets an offer of a job that pays $25,000. Taking the job would raise disposable income by just $4,000, after taking into account the loss of $20,000 in benefits and a 20 percent tax on income over the poverty line. Work related expenses like childcare and transportation could easily eat up that whole amount.

Finally, despite its structural simplicity, a program that topped up income to the poverty line would not necessarily score well on administrative efficiency. It would require periodic reporting of earned income and adjustment of benefits, a task that would be all the harder because the 100 percent benefit reduction rate would provide a strong incentive to hide earnings.

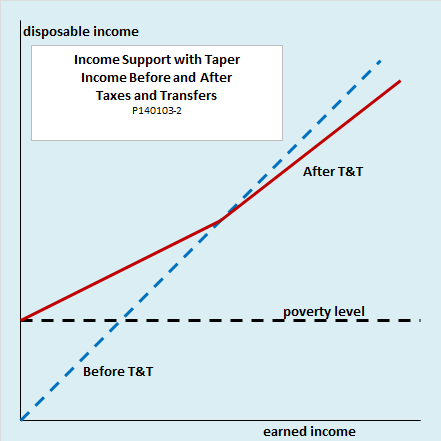

Adding a taper

One way to strengthen work incentives is to taper transfer payments gradually as income increases, rather than cutting them dollar-for-dollar. A tapered benefit was one of the central features of Milton Friedman’s famous negative income tax. Under that proposal, people with no earned income would receive a refundable tax credit, or “negative tax,” sufficient to live on. As their income rose, the amount of the credit would fall by some set percentage of earned income. Once the credit fell to zero, they would start paying pay income tax on any additional earnings.

The next diagram shows a simple version of such a scheme. The basic credit is set at the assumed poverty level of $20,000. The credit is subject to a 50 percent benefit reduction rate until it falls to zero at an earned income of $40,000. Further earnings above that level are subject to a 20 percent income tax.

This scheme, like the flat means-tested grant discussed earlier, is fully effective in lifting everyone at least to the poverty threshold. However, because it is not as narrowly targeted, it is more expensive. Except for those who have no earned income at all, households that would be poor without the program receive more than they need to bring their disposable income up to the poverty line. Also, households that already have enough earnings to escape poverty on their own continue to receive credits until their earnings reach double the poverty level.

Still, the taper substantially improves work incentives compared to a simple top-up scheme, since it lowers the benefit reduction rate to 50 percent from 100 percent. Tinkering with the taper could make work incentives even stronger. For example, under the U.S. government’s earned income tax credit, the poorest families with children receive a cash credit of more than one dollar per dollar earned, making their benefit reduction negative. The benefit reduction rate becomes zero and then positive as income increases, until benefits are eventually phased out altogether.

Friedman maintained that integration of a negative income tax with the existing system of income taxation would avoid the need for a separate bureaucracy, holding down administrative costs. The problem of fraudulent underreporting of income would not completely disappear as long as the benefit reduction rate was greater than zero, but tax administrators already have to be on the lookout for unreported earnings by people at all income levels, and have developed tools for dealing with the problem.

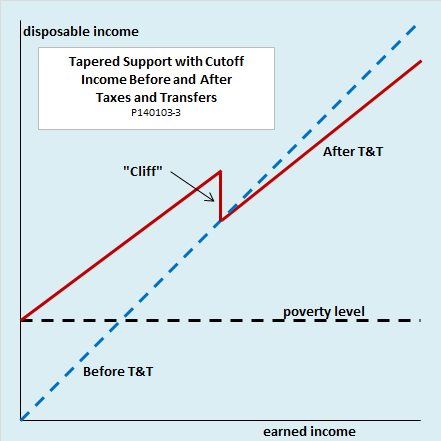

Cutoffs and cliffs

Tapering benefits gradually as income rises helps to maintain work incentives, but it does so at the cost of making the income support program more expensive and less well targeted. Some programs deal with this problem by adding a cutoff beyond which households are no longer eligible for benefits at all. The next diagram shows a simple version of such a cutoff. Here, the benefit reduction rate is just 25 percent rather than the 50 percent of the previous example, but there is a cutoff at double the poverty level, beyond which benefits abruptly fall to zero. A flat-rate income tax of 20 percent applies to still higher incomes.

The problem with this scheme is that it maintains work incentives for households with very low earned incomes but introduces a severe disincentive, or “cliff,” at the cutoff point. For example, a household with earned income of $40,000, double the poverty level, receives $10,000 in benefits, giving it disposable income of $50,000. However, one more dollar of earned income makes the household ineligible for the transfer, so that its disposable income falls to $40,000.80. Earned income has to rise by $12,500 to return disposable income to $50,000.

Benefit cliffs like this one create especially strong disincentives for second workers in a household. For example, imagine a household where one spouse earns 150 percent of the poverty income, or $30,000. Under the program we are looking at, household disposable income, including a $15,000 transfer benefit, would be $45,000. If the other spouse now gets a full-time job that earns 100 percent of the poverty level, or $20,000, household disposable income will rise to just $48,000 ($50,000 less $2,000 tax on earned income over $40,000.) Again, childcare, transportation, and other work-related expenses would erode even that small gain.

Marginal tax rates, cliffs, and work incentives of existing income support programs

High effective marginal tax rates and benefit cliffs like those of our examples are not just theoretical possibilities. They occur in many existing income support programs. The health insurance subsidies provided by the Affordable Care Act are the latest example. A recent New York Times article gives several specific examples. For instance, The Times calculates that a 60-year-old single man living in Decatur County, Georgia, and earning $45,000, would pay just $1,730 a year for the cheapest “bronze” plan after receiving all available subsidies. However, if he earned $5,000 more he would be ineligible for subsidies and would have to pay $8,696 for the same plan. Despite the extra $5,000 earned income, his disposable income, after subsidies and insurance premiums, and even without taking income and payroll taxes into account, would fall by $1,966—an effective marginal tax rate of 139 percent!

Estimating effective marginal tax rates under the many overlapping income support programs in the United States today is a daunting task. One reason is that eligibility, benefits, and cutoffs vary greatly according to family structure, age, and place of residence. Another reason is the way different programs interact with one another.

The general rule is that taxes on earned income and the benefit reduction rates of various programs are additive. For example, if a household faced a 7 percent payroll tax on earned income, a 20 percent benefit reduction rate for food stamps, and a 30 percent benefit reduction rate for Medicaid it would have an effective marginal tax rate of 7 + 20 + 30 percent, or 57 percent.

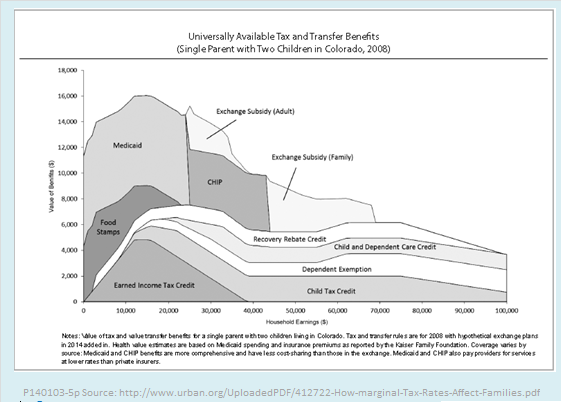

In a recent paper, Elaine Maag, C. Eugene Steuerle, Ritadhi Chakravarti, and Caleb Quakenbush, all of the Urban Institute-Brookings Tax Policy Center, make a heroic effort to estimate effective marginal tax rates for families of various incomes and other characteristics in all fifty states. The following diagram from the paper captures the complexity of the undertaking:

Three conclusions of the study are particularly noteworthy:

- Effective marginal tax rates are moderate for families with earned incomes below the poverty level. For incomes below half the poverty level, effective marginal tax rates for some families are actually negative because of the earned income tax credit.

- Effective marginal tax rates are much higher for families whose earned incomes fall in the range from the poverty level to twice the poverty level. For them, effective marginal tax rates are typically over 50 percent. Rates over 70 percent are not unusual, and rates over 100 percent occur in some cases.

- Effective marginal tax rates are especially high for secondary earners in two-earner households. If childcare, transportation, and other work-related expenses are taken into account, it often does not pay at all for a second member of a low-income household to take a job.

In short, the existing income support system of the United States seems to combine some of the worst features of the stylized alternatives that we illustrated earlier. They are not fully effective; despite their considerable cost, they leave some 16 percent of the population below the official poverty threshold. They are not tightly targeted. In an effort to maintain work incentives, many of them provide benefits to households well above the poverty level. Nonetheless, because of the additive nature of benefit reduction rates for multiple programs, many households, especially those just above and below the poverty level, face cliffs and high effective marginal tax rates that undermine incentives to work. Finally, the complexity of many programs, each run by its own bureaucracy, results in very high administrative expense.

The UBI alternative

By now, the economic appeal of a universal basic income should be apparent. The next diagram shows how a UBI would work, assuming a benefit equal to the poverty level and a 20 percent flat rate tax on all earned income (this time beginning with the first dollar). As before, the diagram illustrates the case of a family for whom the poverty line is $20,000.

A UBI would score well by three of the four criteria by which we evaluate transfer programs:

- It would be effective in raising household incomes at least to the poverty level (as long as the benefit is set at that level or higher).

- It would provide substantial work incentives. Because there is no reduction of benefits as earned income rises, it would avoid the problems of cliffs and high effective marginal tax rates for low-income households and second earners. (For readers familiar with the economic terms, a UBI would have an “income effect” on labor supply but no “substitution effect,” unlike current income support programs, which typically have both.)

- It would be administratively efficient. It would require no verification of any personal characteristic or behavior other than the existence of the beneficiary. The program could be integrated with the existing federal tax system. For example, households in the class for whom the poverty line is $20,000 would receive the full $20,000 in cash only if they had no earned income. Those with earned income from $1 to $100,000 would receive a payment equal to $20,000 minus taxes due, that is, minus 20 percent of their earned income. Those earning more than $100,000 would get a credit of $20,000 toward taxes due.

Unlike other income support programs, however, a universal basic income, by its nature, is completely untargeted. To its supporters, that is its essential virtue. Precisely because it is universal and untargeted, it minimizes disincentives to work and facilitates administrative efficiency. To its detractors, however, universality is a fatal flaw that would make a UBI unaffordable.

But would a UBI really be unaffordable? Yes, it would be a large-scale fiscal operation. Providing a grant to each individual that was sufficient to bring a family of three above our assumed $20,000 poverty line would require payments or tax credits totaling roughly 10 percent of GDP. That would be unaffordable if the UBI were simply layered on top of today’s system of taxes and transfers. But that is not what UBI supporters propose.

A UBI would make sense only as part of a thorough overhaul of today’s tax and transfer systems. For the poor, the UBI would replace other transfer programs that now impose crippling disincentives to work while still leaving many households in poverty. For middle and upper income groups, it would replace many if not all of the existing deductions, credits, exclusions and preferences that are part of the personal income tax. If the tax and transfer system as a whole were properly restructured, say UBI proponents, it would provide income support that was better targeted toward the poor without raising marginal rates for middle class and wealthy taxpayers.

A critical examination of that claim will require a detailed review of the transfer programs and tax breaks that a UBI could replace. That will be the subject of the next post in this series.

Go to Part 2 of this series, “Could We Afford a Universal Basic Income?”