The Washington Post‘s Catherine Rampell devoted a column (12/24/15) to a popular Washington pastime: trying to get young people angry at their parents and grandparents so that they are not bothered by the enormous upward redistribution of income taking place in this country.

She begins the piece by telling readers that college students are wasting their time complaining about diversity issues and sensitivity to racism and sexism, then gets to the meat of the story:

Older generations have racked up trillions in debt and stuck young people with the bill. This is not just due to expensive wars, unfunded tax cuts, Keynesian financial interventions and the other usual scapegoats for fiscal profligacy.

One of the largest ongoing sources of spending involves huge age-specific transfers: Our politicians are paying off older, higher-voter-turnout Americans in the form of generous benefits that those older people have not paid for and never will. Which means the tab will need to be picked up by someone else—i.e., someone younger.

For example, a married couple with a single breadwinner who earned the average wage his whole life and turned 65 this year will collect more than six times as much in net Medicare benefits as the couple paid out in taxes. That’s after taking into account both Medicare premiums and other ways the couple could have invested their payroll tax money.

“Invincible” youngsters are subsidizing health care for their not-yet-Medicare-eligible elders on the individual insurance market as well. And elsewhere on government balance sheets, spending on the old is crowding out spending on the young. At the state level, politicians have responded to swelling pension obligations by disinvesting from public higher education. These funding cuts have then been offset with massive tuition hikes—which fall to, you guessed it, today’s college students.

Fiscal issues of course aren’t the only way that young people have been done wrong by their elders. The warming of our planet and some politicians’ promisesto undermine what small progress has been made to curb climate change also come to mind.

There is so much wrong here that it hard to know where to begin. Let’s start with an easy one, the story of Medicare and Social Security.

Lesson One: Social Security and Medicare Are Not Unfair to the Young

First, Rampell’s comparison is misleading, since there are few married couples with single breadwinners turning age 65. Most women have been in the workforce for the last four decades. If we look to the same study referenced by Rampell, and take the more typical case of a couple with an average earner and low earner, we find that the value of the Medicare benefit is roughly four times (rather than six times) the taxes paid.

Most of the reason the value of Medicare benefits exceeds the value of the taxes paid is not the generosity of the benefits received by our seniors. The main cause is the fact that we pay our doctors twice as much as doctors in Canada, Germany and other wealthy countries. We also pay twice as much for our drugs and medical equipment. This is a case of upward redistribution from the rest of us to members of the 1 Percent. (Almost all doctors are in the richest 1 or 2 percent of the income distribution.) But rather than talking about how the rich raise the cost of our healthcare, Rampell wants us to be upset at seniors.

If we take Social Security and Medicare taxes together, the story is more balanced, although the ratio of benefits to taxes is still close to two to one, with total lifetime imbalance of $447,000 (in 2015 dollars) for this couple. Before we shed too many tears for today’s young ones, it is worth noting that the same study projects the imbalance of benefits and taxes to rise to more than $1.1 million (in 2015 dollars) for today’s 25-year-olds.

If that is hard to understand, imagine we told our adult children to give us $100,000 to support our retirement and then to get that money back from their children, who will in turn get the money back from their children, etc. This is the basic story of Social Security and Medicare. If this greatly troubles you, then you should be extremely mad at the generation who lived through the Great Depression and fought World War II. They really made out like bandits from these programs because they paid very little money in taxes compared to the benefits collected, as can be seen in this same study.

I could go on to mention that many older people live with their children and grandchildren. How does cutting benefits in that story help the young? Social Security also provides survivors and disability benefits that often help the young, but let’s move on.

Lesson Two: The Affordable Care Act Redistributes from the Healthy to the Less Healthy, not the Young to the Old

Rampell gives yet again the long-deflated “young invincible” story about how the Affordable Care Act (ACA) relies on healthy young people to pay premiums to support the cost of providing care to older less healthy people. While there is a modest skewing of premiums against the young, the main story of the ACA is that it relies on the healthy of all ages to subsidize the less healthy.

The Kaiser Family Foundation did an analysis two years ago that showed that even an extreme skewing by age only raised the cost of the program by around 2 percent. The big problem for the ACA is if there is a skewing by health conditions.

It is important to recognize that there are a large number of people of all ages with near zero healthcare expenditures. The older people in the exchanges (ages 55 to 64) pay premiums that average three times as much as the premiums paid by younger people. If the healthy people in both age groups get almost nothing back in benefits, the older healthy people are paying three times as much to the support the ACA as the young people. Should we shed more tears for the 20-somethings?

Lesson Three: Our Children Will Only Be Hurt by the Debt Because the Washington Post and Other Elite Types Will Use it As An Excuse to Cut Necessary Spending

OK, 20-somethings, how do you know about our massive debt? Yeah, it’s more than $18 trillion, can you feel it?

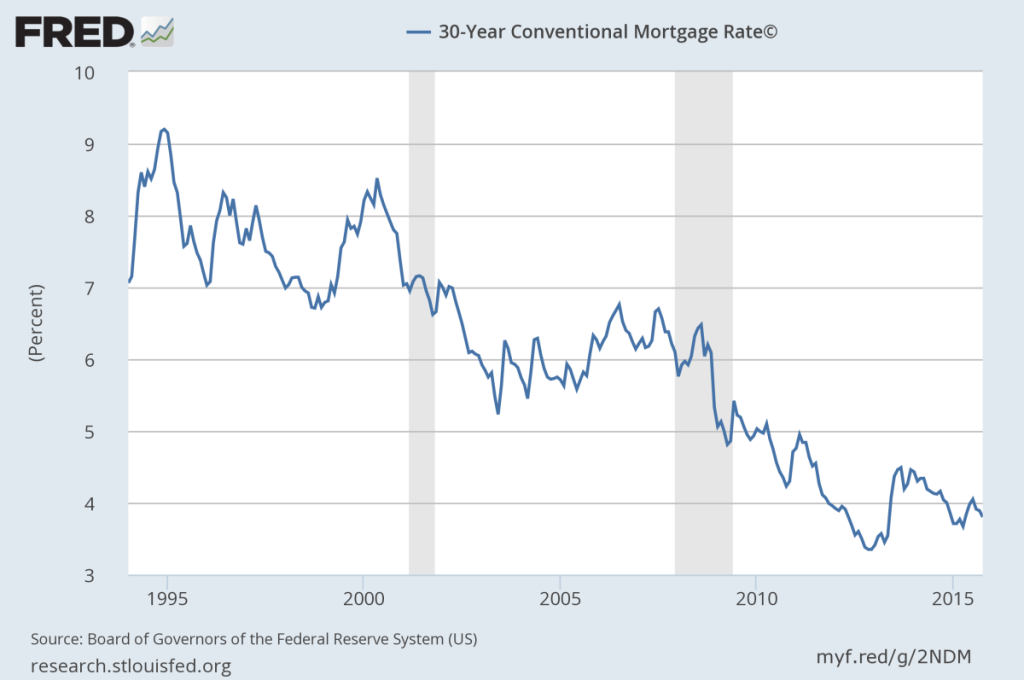

You surely can’t feel it from its economic impact. Interest rates in the economy are at their lowest level in more than half a century. Thirty-year mortgage rates are hovering near 4 percent. They were generally in the 6 percent range back at the end of the 1990s, when we were running budget surpluses and making plans to pay off the debt. Interest rates on car loans, student loan debt and credit card debt are correspondingly lower today.

How about the raging inflation caused by the debt? Well, the Federal Reserve Board has been working hard to raise the inflation rate back towards its 2.0 percent target.

What about the enormous amount of money that has to be diverted from other spending to meet the interest burden? Current interest costs, net of payments from the Federal Reserve Board, come to less than 1 percent of GDP. By comparison, the interest burden was more than 3 percent of GDP in the early 1990s. (That’s what lower interest rates will do.) If a 20-something claims that they can feel the economic impact of the debt, it is time for some serious drug testing.

Now, there is clearly a political impact. The Washington Post, along with other Very Serious People, has hyped the debt endlessly. They have raised fears over the debt to prevent spending that would both help boost the economy back to full employment and meet our needs in areas like education, infrastructure, research and development, and addressing global warming. The damage done by the Very Serious People’s scare stories about the deficit is in fact a very big deal. But it is a bit over the top to blame this one on the older generation as an age group, even if most of the Very Serious People gang is older.

Lesson Four: We Hand Our Children a Whole Economy, Not Just Government Debt

One of the most bizarre inventions of the Very Serious People is the idea that somehow generational issues can be measured by government indebtedness and taxation. We expect people to get wealthier through time as technology advances, and we become better educated and have a better and more advanced infrastructure and capital stock. The well-being of our children and grandchildren will depend on the whole economy and society we hand them; the tax burdens associated with the government debt, or even the cost of Social Security and Medicare benefits, are a trivial part of the picture.

If that sounds hard to understand, let’s try a simple thought experiment. Suppose we snap our fingers and eliminate completely every tax burden for the young associated with us old-timers. That means we not only get rid of the government debt, but we also zero out their Social Security and Medicare tax liability. Sounds great–we’ve really done right by our young now.

OK, now let’s also get rid of all the technological breakthroughs of the last 35 years. There are no smartphones or even cell phones. There is no Internet and only the most clunky of personal computers. (Apple wasn’t even cool back then.) Music is still available only on cassettes and vinyl records. Life expectancy is much shorter, as we don’t have many of the treatments that have been developed in the last three decades. And there is no Uber.

So, are our kids better off now? I doubt most people would say yes, especially not the 20-somethings.

If we want to seriously discuss whether we are making things better or worse for our kids, then we have to ask about the whole economy and society we pass on to them. When we force many of our kids to grow up with parents who are unemployed and/or in poverty because the Very Serious People won’t let us spend the money necessary to make them employed and let them have decent jobs, this is a huge issue of generational equity. The same applies to inadequate spending on infrastructure and education. Also, messing up the planet with greenhouse gas emissions is a really huge deal (addressed more below). But none of these factors gets picked up in the national debt.

There is one more point that the Very Serious People need to have beaten into their heads. Tax dollars are only one way in which the government pays for things. We pay for a large and growing number of items with government-granted monopolies in the form of patents and copyrights. These monopolies raise the cost of everything from drugs and medical equipment to seeds and recorded music by many hundreds of billions of dollars above the free-market price.

From the standpoint of our children, it makes no difference if we impose an $80,000 tax on a drug like Sovaldi, and use the money to finance drug research, or if we give Gilead Sciences a patent monopoly that allows it to charge a price that is $80,000 above the free-market price. Media outlets like the Post (which gets lots of advertising dollars from pharmaceutical companies) have been very effective in focusing attention exclusively on tax dollars and ignoring all the other ways in which the government directs money and resources. (On a related matter, do you recall any discussion of the $4 billion given to Jeff Bezos by exempting Internet retailers from the requirement to collect the same sales tax as their brick-and-mortar competitors?)

Lesson Five: Global Warming Threatens the Planet, but It Is the Fault of the Rich, not Older Generations

Rampell is absolutely right that young people should be mad about global warming, but absolutely wrong about the direction of blame. The science on global warming has been compelling for two decades. Yet media outlets like the Washington Posthave treated deniers like House Speaker Paul Ryan or the Republican crop of presidential candidates as serious people.

These papers know how to go after people when they are not telling the truth. Think of how they went after Bill Clinton to get to the bottom of his sexual relationship with Monica Lewinsky. They asked him and his staff day after day about the details and the inconsistencies in Clinton’s denials. They should go after top Republicans with the same vigilance on global warming; writing stories every day about how Paul Ryan continues to deny science that is accepted by virtually every expert in the field. They should point out to readers that the man is either an incredible fool or an outright liar. No media outlet ever does this, because, hey, that would be partisan.

Sorry, Ms. Rampell, this Baby Boomer is not taking the blame for the failings of your wealthy employer. The Post and other major news outlets have enormously failed the country in their coverage of global warming, but like the overwhelming majority of people of my generation, I don’t own a news outlet. So if you want to be honest in directing anger, use your next column to tell the world what an awful person your employer is. We look forward to that one.

Economist Dean Baker is co-director of the Center for Economic and Policy Research in Washington, DC. A version of this post originally appeared on CEPR’s blog Beat the Press (12/24/15).

Messages can be sent to the Washington Post at letters@washpost.com, or via Twitter @washingtonpost. Please remember that respectful communication is the most effective.